![]()

06 APRIL 2026

This week’s edition unfolds against a strategic backdrop in which Asia is being shaped not only by open confrontation, but by the increasingly political management of access, alignment, and vulnerability. Taiwan’s opposition is reopening direct political contact with Beijing even as Taipei’s defence budget deadlock begins to affect military readiness, while China’s sanctions on a Japanese lawmaker over Taiwan ties show how cross-strait tensions are spilling more openly into the region’s wider diplomatic relationships. What emerges is a landscape in which deterrence is no longer being tested only through military pressure, but also through political channel-building, domestic division, and selective coercion.

At the same time, this issue shows that Asia’s strategic environment is being reshaped by forces that extend well beyond the Taiwan Strait. Pakistan’s renewed border violence with Afghanistan has complicated its effort to present itself as a diplomatic broker in the Iran war, exposing the gap between regional ambition and internal fragility. India’s unusual Hormuz transit, meanwhile, underlines how one of Asia’s most critical energy corridors is no longer functioning as an open commercial route, but as a space of conditional passage governed by wartime discretion. The result is a region still deeply exposed to external shocks, yet increasingly forced to navigate them through improvised and politically unequal arrangements.

Yet this issue is also about strategic adaptation—and about which actors are trying to turn disruption into advantage. South Korea and France are giving their bilateral relationship more operational substance by tying energy security, defence cooperation, and advanced technology into a single strategic framework, while China is using its outreach to Europe to reinforce its ceasefire diplomacy and present itself as a responsible external actor. In parallel, Europe’s rare parliamentary visit to China shows that engagement is continuing, but under harder terms shaped by digital trade frictions, product safety concerns, and growing demands for reciprocity.

Taken together, the developments in this issue point to an Indo-Pacific that is becoming more politically fragmented, more technologically strategic, and more tightly connected to crises beyond its immediate borders. From Japan’s effort to anchor semiconductor and AI capacity more firmly within a national security framework to the widening entanglement of cross-strait politics with broader regional diplomacy, the region’s central question is no longer simply how to deter conflict, but how to manage interdependence under pressure.

- Key Developments

- Statistics of the Week

- Map of the Week

- Photo of the Week

- Infographic of the Week

- Regional Alliances

- Analysis

Taiwan Opposition Chief’s China Visit Rekindles Cross-Strait Political Channel

Taiwan’s main opposition party, the Kuomintang (KMT), said its chairwoman Cheng Li-wun will visit China from April 7 to 12 after accepting an invitation from Xi Jinping, with stops planned in Beijing, Shanghai and Jiangsu. The trip is notable because Beijing continues to refuse formal contact with President Lai Ching-te’s government, which it brands “separatist,” while maintaining regular engagement with senior KMT figures instead. Cheng has cast the visit as an effort to promote “cross-strait peace and stability” and rebuild mutual trust.

The timing gives the trip added political weight. It comes as Lai’s government is struggling to push an extra $40 billion defence package through an opposition-controlled parliament, with the KMT saying it supports stronger defence but will not sign “blank cheques” without more detail. It also precedes U.S. President Donald Trump’s planned mid-May visit to China, underscoring how cross-strait politics, Taiwan’s domestic budget fight, and wider U.S.-China diplomacy are becoming increasingly entangled rather than separate tracks.

Pakistan’s Border Clash with Afghanistan Complicates Its Mediation Ambitions

Pakistan and Afghanistan traded heavy artillery and other fire on March 29, only days after both sides had announced a temporary pause in fighting, underscoring how fragile the latest de-escalation effort has become. Officials said the exchanges hit Afghanistan’s Kunar province and Pakistan’s Bajur district, with Kabul claiming Pakistani fire killed at least one person and wounded 16 others, mostly women and children. Pakistani officials denied targeting civilians and said they were responding to shelling from the Afghan side. The renewed violence follows the worst fighting in years between the two neighbours last month, including a disputed Pakistani strike in Kabul that Afghan authorities said killed more than 400 people at a drug rehabilitation centre.

The timing is strategically awkward for Islamabad because the clashes came as Pakistan sought to present itself as a diplomatic broker in the Iran war. Reuters reported that the border fighting occurred on the same day Pakistan hosted regional powers for talks on Middle East de-escalation and signalled that it could host potential U.S.–Iran negotiations in the coming days. The contrast is stark: Pakistan is trying to project regional diplomatic relevance abroad while still struggling to contain a dangerous conflict on its own western frontier.

China Sanctions Japanese Lawmaker Over Taiwan Ties, Escalating Bilateral Tensions

China has imposed sanctions on Japanese lawmaker Keiji Furuya, accusing him of “colluding with Taiwan independence forces,” in the latest escalation of tensions over Taiwan. According to state media, the measures include a ban on entering China and the freezing of any assets he may hold in the country. Furuya, a senior figure in Japan’s ruling Liberal Democratic Party and head of a parliamentary group promoting ties with Taiwan, recently visited Taipei and met President Lai Ching-te, prompting a sharp response from Beijing. Japan condemned the move as “unacceptable” and demanded its reversal, highlighting the diplomatic fallout.

The significance of the sanctions lies less in their practical impact—Furuya himself said he has no assets in China—than in their political signalling. Beijing is reinforcing Taiwan as a non-negotiable “red line” while expanding its use of targeted punitive measures against foreign individuals, not just governments. This fits a broader pattern of economic and diplomatic pressure on Japan, including export controls and earlier sanctions tied to Taiwan-related disputes. The episode therefore underscores how cross-strait tensions are increasingly spilling into China–Japan relations, turning individual political engagement with Taiwan into a direct trigger for interstate friction.

German Firms Face Strategic Squeeze Between the United States and China

German companies are deeply entangled with both the United States and China, making any serious attempt at economic decoupling highly costly. A study by the University of Sussex and King’s College London, seen by Reuters, found that exposure runs across the DAX and MDAX indices through sales, production, research, and supply chains. Automakers and machinery firms are especially reliant on China as a market, while chemical and pharmaceutical groups depend more heavily on the United States for research, development, and production. Digital, telecoms, and semiconductor firms, meanwhile, remain exposed to suppliers in both countries.

The significance is broader than corporate balance sheets. The findings underline how difficult it has become for Berlin to craft a clean economic strategy as U.S.-China tensions intensify. Reuters notes that BMW generates more revenue from China than from the United States while also relying heavily on Chinese battery inputs, and Siemens draws substantial revenue from both markets. The result is not simple interdependence but strategic constraint: German industry was built in a globalised system that now collides with geopolitical rivalry, leaving Berlin caught between its security alignment with Washington and its commercial exposure to China.

U.S. Senator Uses Hong Kong Warning to Press Taiwan on Defence Resolve

U.S. Senator John Curtis warned during a visit to Taipei that Taiwan should look at what happened in Hong Kong and “not be naive” about China’s intentions, using Beijing’s 2020 national security law in the former British colony as a cautionary example for the island. Curtis and Democratic Senator Jeanne Shaheen met President Lai Ching-te as part of a bipartisan delegation focused on Taiwan’s security and the island’s stalled defence spending debate. Curtis said Taiwan needed open and serious discussion about the threat it faces, while Shaheen pointed to growing Chinese military pressure around the island.

The visit is significant because it linked Taiwan’s domestic budget deadlock more directly to wider U.S. concerns about deterrence credibility. Reuters reported that Lai’s proposed extra $40 billion defence package remains stuck in an opposition-controlled parliament, even as U.S. lawmakers urged faster movement and Washington prepared a further arms package for Taipei. The intervention also came as Beijing maintained outreach to Taiwan’s opposition Kuomintang while rejecting contact with Lai’s government, underscoring how cross-strait pressure is being applied through both military coercion and political channel-building.

China Backs Pakistan’s Iran Diplomacy with a Joint Five-Point Peace Plan

China and Pakistan have moved to give Islamabad’s Iran-war diplomacy wider backing by jointly proposing a five-point plan calling for an immediate ceasefire, a quick start to peace talks, protection of civilians and critical infrastructure, respect for the sovereignty and territorial integrity of Iran and other Gulf states, and the restoration of safe commercial navigation through the Strait of Hormuz. The initiative was announced after talks in Beijing between Chinese Foreign Minister Wang Yi and Pakistani Foreign Minister Ishaq Dar, with Beijing also saying it would strengthen coordination with Pakistan on the crisis.

The move is significant because it brings China more visibly behind Pakistan’s attempt to position itself as a diplomatic intermediary without committing Beijing to any direct mediating role of its own. China retains major interests in Gulf energy flows and regional stability, but its language remains carefully calibrated around de-escalation, sovereignty, and shipping security rather than coercive diplomacy. That makes the joint plan less a breakthrough than a coordinated effort to shape the diplomatic agenda—and to show that Beijing sees value in Pakistan acting as a politically useful front-line broker in a conflict China still prefers to manage at arm’s length.

India’s Unusual Hormuz Exit Highlights Selective Access and Maritime Risk

An Indian-flagged LPG tanker, Pine Gas, reached the Arabian Sea only after taking an unusual route through the Strait of Hormuz under Iranian direction, highlighting the improvised conditions now governing one of Asia’s most critical energy corridors. Reuters reports that after waiting nearly three weeks amid missile and drone activity, the vessel was cleared on March 23 to pass not through the normal shipping lanes but via a narrow channel north of Iran’s Larak Island, because the regular route had been mined. The tanker’s 27 Indian crew all had to consent before sailing, and Indian naval vessels then escorted it after transit.

The episode matters because it shows that access through Hormuz is no longer open in any normal commercial sense, but increasingly subject to selective political and military control. Reuters says Iran has allowed passage for “friendly nations” such as India, China, Russia, Iraq and Pakistan, and that six Indian ships have exited, while 18 Indian-flagged vessels with about 485 Indian seafarers remain trapped in the Gulf. For India, heavily dependent on imported LPG for household cooking, this is not just a shipping story but a sharp reminder of how energy security is now exposed to wartime discretion and chokepoint coercion.

TSMC’s 3nm Japan Plan Pushes Advanced Chipmaking Deeper into the Indo-Pacific

TSMC plans to begin equipment installation and mass production of 3-nanometre chips in 2028 at its second factory in Japan, according to a Taiwanese government filing reported by Reuters. The new plan marks a significant upgrade from the company’s earlier Japan strategy, which focused on more mature process technologies. Under the revised blueprint, the second plant will have monthly capacity of 15,000 12-inch wafers using the advanced 3nm process, while TSMC’s first Kumamoto fab has already begun volume production. Reuters also noted that the company previously said total investment in its first two Japanese fabs would exceed $20 billion.

The shift matters because it gives Japan a more serious role in the geography of advanced semiconductor production rather than limiting it to legacy-node manufacturing. That has clear strategic significance for Tokyo’s effort to rebuild domestic chip capability and reduce supply-chain vulnerability, while also advancing broader U.S.-aligned efforts to diversify high-end semiconductor production beyond Taiwan. It does not put Japan at the cutting edge of TSMC’s most advanced global output, but it does narrow the gap and strengthens the country’s position in the region’s increasingly security-sensitive semiconductor landscape.

Taiwan Warns Budget Delay Is Starting to Hit Military Readiness

Taiwan’s defence ministry has warned that delays in approving the 2026 general budget are threatening T$78 billion ($2.44 billion) in military spending, disrupting the original timetable for weapons procurement, maintenance, and training. A senior ministry official said the hold-up would prevent the armed forces from executing about 21% of this year’s planned budget on schedule, affecting programmes including U.S.-made HIMARS systems, Javelin missile procurement and replenishment, and F-16 training. The proposed 2026 defence budget totals T$949.5 billion, a 22.9% increase that would lift spending to 3.32% of GDP—the highest share since 2009.

The significance is not merely procedural. The warning shows that Taiwan’s defence debate is no longer only about future spending levels, but about immediate readiness costs caused by political deadlock. The delay comes as Taipei is also struggling to pass a separate $40 billion special defence package through an opposition-controlled parliament, even while U.S. lawmakers have urged faster action and Washington says it is trying to accelerate delayed arms deliveries. The result is a growing gap between Taiwan’s stated urgency about the China threat and its ability to translate that urgency into timely military execution.

Taiwan Opposition Leader Frames China Trip as a Bid to Avert Cross-Strait Crisis

Taiwan opposition leader Cheng Li-wun said ahead of her China visit that “the world does not need a crisis over Taiwan,” casting the trip as an effort to promote peace and reconciliation at a time of mounting cross-strait tension. Cheng, chairwoman of the Kuomintang (KMT), is due to travel to China for six days from April 7 at Xi Jinping’s invitation, with stops in Beijing, Shanghai and Jiangsu. Beijing continues to refuse contact with President Lai Ching-te’s government, which it denounces as “separatist,” while keeping political channels open with the KMT instead.

The visit is politically significant because it highlights the widening gap between Taiwan’s two main approaches to China: Lai insists only Taiwan’s people can decide the island’s future, while the KMT argues that dialogue is needed to reduce the risk of military crisis. It also comes as Taiwan’s opposition-controlled parliament continues to hold up Lai’s proposed $40 billion supplemental defence budget, giving the trip added domestic weight. Beijing has used the moment to renew its “peaceful reunification” messaging, but public support in Taiwan for Chinese sovereignty remains minimal.

EU Lawmakers Use Rare China Visit to Press on E-Commerce Safety and Market Access

A nine-member European Parliament delegation has begun the bloc’s first parliamentary visit to China in eight years, using meetings in Beijing and Shanghai to press Chinese officials over unsafe consumer goods, forced labour concerns, and the limited access European firms face in the Chinese market. Reuters reports that the lawmakers, led by Internal Market Committee chair Anna Cavazzini, raised the “high influx of dangerous and non-compliant products” entering the EU from China, just days after Brussels agreed to overhaul customs rules and tighten scrutiny of low-value parcels sold through platforms such as Shein, Temu and AliExpress.

The visit matters because it reflects a harder European line on China’s e-commerce and digital footprint even as both sides try to stabilise broader ties. The European Parliament said the delegation would focus on digital regulation, consumer protection, and fair competition, while meeting Chinese regulators, lawmakers, the EU Chamber of Commerce, and major platforms including Shein, Alibaba and Temu. China has welcomed the trip as a chance to improve relations after lifting sanctions last year on several EU lawmakers, but the substance of the visit shows that Brussels is increasingly linking trade engagement to product safety, regulatory compliance, and economic reciprocity.

South Korea and France Elevate Ties as Energy Shock and Security Pressures Converge

South Korea and France agreed on April 3 to upgrade their relationship to a “global strategic partnership” during President Emmanuel Macron’s state visit to Seoul, the first by a French president since 2015. The two sides said they would deepen cooperation in defence, aerospace, advanced technology, critical minerals, semiconductors, quantum technology, nuclear energy, and offshore wind, while also aiming to raise bilateral trade to $20 billion by 2030 from $15 billion in 2025. Seoul also highlighted agreed memoranda involving Korea Hydro & Nuclear Power and France’s Orano and Framatome to strengthen nuclear fuel supply chains and support possible joint entry into overseas nuclear markets.

The timing gives the upgrade broader strategic weight. Lee Jae Myung and Macron explicitly linked their partnership to the economic and energy disruption caused by the Iran war and agreed to cooperate on securing safe maritime transport through the Strait of Hormuz. Macron also said the two countries, both major arms producers, would seek more joint exercises, production cooperation, and stronger “strategic depth” in military capabilities. The result is not a formal alliance, but a clearer attempt to bind energy security, defence-industrial cooperation, and Indo-Pacific diplomacy into a more substantive bilateral framework.

China Uses Europe Talks to Reinforce Ceasefire Push on the Middle East

China used separate calls with EU foreign policy chief Kaja Kallas and German Foreign Minister Johann Wadephul to press again for a ceasefire in the Middle East, linking an end to the fighting directly to safer navigation through the Strait of Hormuz. According to Reuters, Foreign Minister Wang Yi told Kallas that “a ceasefire is the key” to restoring safe passage and urged all parties to build broader consensus for a prompt end to the war. In his call with Wadephul, Wang said China and Germany, as “responsible major countries,” should take an objective and impartial stance and play a constructive role.

The significance lies in how Beijing is positioning itself. China is not offering robust mediation or direct intervention; it is widening its diplomatic outreach while framing ceasefire diplomacy, Gulf sovereignty, civilian protection, and maritime security as linked issues. Reuters notes that China has condemned U.S.-Israeli strikes on Iran as violations of international law, but Wang’s latest remarks also added pressure on Tehran by calling for negotiations and protection of shipping routes. The result is a familiar Chinese approach: present itself as a responsible diplomatic actor while avoiding deeper entrapment in the conflict.

Microsoft’s Japan Investment Ties AI Expansion More Closely to Economic Security

Microsoft said it will invest 1.6 trillion yen ($10 billion) in Japan between 2026 and 2029 to expand AI infrastructure and deepen cybersecurity cooperation with the government, in one of the country’s largest recent foreign technology commitments. The plan includes training 1 million engineers and developers by 2030 and expanding Japan-based AI computing capacity with domestic partners including SoftBank and Sakura Internet, allowing companies and government agencies to keep sensitive data inside Japan while using Microsoft Azure services.

The move matters because it links commercial AI expansion directly to national resilience. Microsoft said it will also deepen cooperation with Japanese authorities on sharing intelligence related to cyber threats and crime prevention, aligning the investment with Prime Minister Sanae Takaichi’s push to strengthen growth through advanced strategic technologies while protecting national security. Reuters also notes that around one in five working-age people in Japan now use generative AI tools and that the country faces a projected shortfall of more than 3 million AI and robotics workers by 2040. The result is not just more data capacity, but a broader effort to anchor advanced digital infrastructure and cyber defence more firmly within Japan.

China’s Mediation Push Gains Traction in Pakistan–Afghanistan Conflict

China said negotiations between Pakistan and Afghanistan are “advancing steadily,” signaling some momentum in its effort to mediate the worst fighting between the two neighbours since the Taliban returned to power in 2021. Reuters reported that Chinese Foreign Ministry spokesperson Mao Ning said both Islamabad and Kabul welcome Beijing’s mediation and are willing to sit down for talks again, though she did not confirm the venue; earlier reports had pointed to Urumqi in China’s northwest as the likely location.

The development matters because it shows China trying to convert geographic proximity into diplomatic influence at a moment of acute regional instability. Beijing shares a border with both countries and has stepped up engagement in recent weeks through calls with their foreign ministers and visits by a special envoy. The conflict, which began in October, has killed scores on both sides, with Afghanistan bearing the heavier toll, while Pakistan continues to accuse the Afghan Taliban of sheltering militants behind attacks in Pakistan, a charge Kabul denies. China is therefore positioning itself not simply as an observer, but as a regional crisis manager seeking to stabilise a conflict on its western periphery.

Japanese-Linked LNG Tanker Crosses Hormuz, Signalling a Fragile Reopening

A Japanese-linked LNG tanker has crossed the Strait of Hormuz, marking the first Japan-connected vessel and the first LNG carrier known to transit the chokepoint since Iran effectively shut it after the U.S.-Israeli strikes in late February. Reuters reported that Sohar LNG, co-owned by Mitsui O.S.K. Lines, made the passage as Iran continued allowing ships it considers unconnected to the United States or Israel to leave the Gulf. Shipping data also showed Omani-operated tankers and a French-owned container ship crossing, with some vessels apparently switching off identification signals during transit.

The development matters because it suggests not a genuine reopening of Hormuz, but a highly selective and politically controlled easing of passage. Reuters notes that about 45 ships owned or operated by Japanese companies were still stranded in the region as of early April, underscoring how limited the breakthrough remains. For Japan and other Asian importers, the crossing is therefore less evidence of restored normality than of a precarious corridor governed by wartime discretion, nationality signalling, and continued maritime risk.

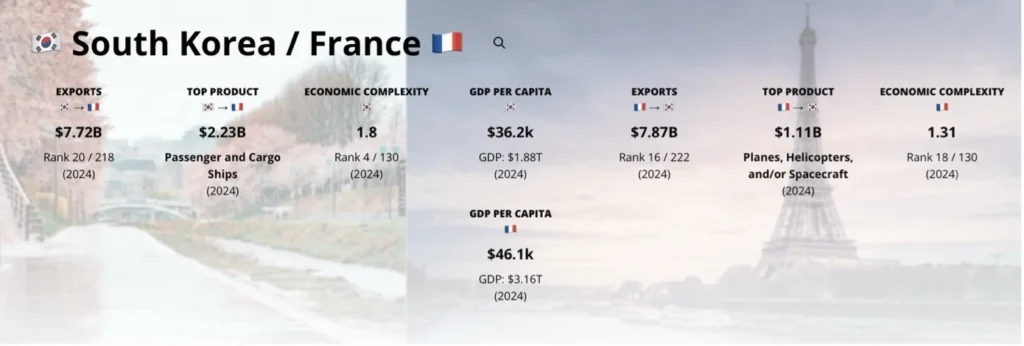

South Korea–France Economic Ties: Scale, Structure, and Strategic Complementarity

The economic relationship between South Korea and France reflects a mid-sized but structurally significant partnership anchored in high-value industrial exchange rather than sheer volume. According to data from the Observatory of Economic Complexity, South Korea exported approximately $7.7 billion worth of goods to France in 2024, while France exported around $7.8 billion to South Korea, indicating a broadly balanced bilateral trade relationship. What stands out is not the size, but the composition: South Korea’s top export to France is passenger and cargo ships (around $2.23 billion), while France’s leading export to Korea is aerospace products, including aircraft and helicopters (around $1.11 billion). This points to a relationship centred on capital-intensive, technologically advanced industries rather than consumer trade.

The broader economic indicators reinforce this complementarity. South Korea ranks higher in economic complexity (1.8, 4th globally), reflecting its highly diversified and advanced export base, while France’s slightly lower score (1.31) is offset by higher income levels, with GDP per capita at roughly $46,100 compared to South Korea’s $36,200. This asymmetry is instructive: Korea brings industrial depth and manufacturing capability, while France offers higher-value markets, aerospace leadership, and financial scale. The result is a partnership that is not defined by dependency, but by mutual specialisation—precisely the kind of economic alignment that can be leveraged more strategically as both countries deepen cooperation in defence, energy, and advanced technologies.

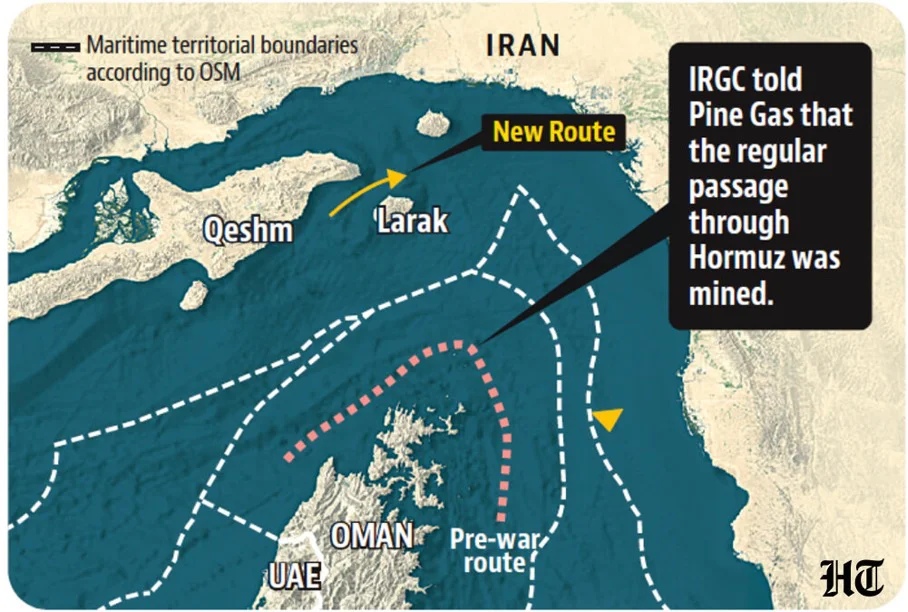

Hormuz Under Wartime Control: The Geography of Selective Passage

This week’s map highlights the altered geography of maritime access through the Strait of Hormuz following the escape of the Indian-flagged LPG tanker Pine Gas. Rather than using the regular commercial passage, the vessel was directed through a narrow alternative route north of Iran’s Larak Island after being told that the normal channel had been mined. The visual makes clear that the issue is not merely congestion or heightened risk, but the physical restructuring of passage itself. By contrasting the pre-war shipping route with the improvised new corridor, the map shows how one of the world’s most important energy chokepoints is now being managed under conditions of military disruption and political discretion.

What makes the map significant is that it illustrates a shift from open commercial transit to selective access controlled by force. Passage through Hormuz is no longer governed primarily by established maritime routines, but by wartime decisions over who may leave, by which route, and under what protection. That matters especially for Asian states such as India, whose energy security remains heavily exposed to Gulf shipping. The map therefore captures more than a navigational adjustment. It shows how coercion at a chokepoint can redraw the practical geography of trade, turning a global shipping lane into a corridor of conditional and politically mediated access.

Macron and Lee Raise a Toast: Symbolism of a Strategic Partnership in Motion

This week’s image captures French President Emmanuel Macron and South Korean President Lee Jae Myung, alongside their spouses, raising a toast during a state dinner at the Blue House in Seoul—an event marking Macron’s first state visit to South Korea since 2015. The setting blends formal diplomacy with carefully curated symbolism: Korean and French cuisine were served together, accompanied by wine and traditional liquor, reflecting an effort to present bilateral ties as both culturally grounded and forward-looking. Macron’s use of Korean phrases during the toast and the presence of leading business and cultural figures further reinforced the performative dimension of the occasion, projecting warmth and mutual respect.

The image matters because it illustrates how diplomacy is being staged to support a broader strategic shift. The dinner took place alongside an agreement to elevate relations to a “global strategic partnership,” linking cooperation across defence, energy, and advanced technology sectors. The visual—leaders in a moment of conviviality—therefore contrasts with the harder geopolitical context behind it: energy disruption from the Iran war, growing Indo-Pacific security tensions, and Europe’s effort to establish a more tangible regional role. The toast is not merely ceremonial; it signals an attempt to translate political alignment into a deeper and more operational partnership.

EU–China Digital Trade Frictions: Consumer Protection Meets Market Access

This week’s infographic highlights the European Parliament’s first visit to China in eight years, centring on digital trade, consumer protection, and fair competition. The visual combines imagery of EU lawmakers, trade flows, and e-commerce platforms to illustrate a core concern: the overwhelming volume of low-value parcels entering Europe, most of them from China. As Reuters reports, more than 5.8 billion such parcels entered the EU in 2025, with over 90% originating from China, placing significant strain on customs enforcement and product safety systems. The graphic captures this imbalance by linking Chinese e-commerce exports directly to regulatory pressure within the EU.

The infographic is significant because it makes clear that the issue is not simply trade volume, but regulatory asymmetry. By highlighting unsafe or non-compliant goods, strained customs systems, and uneven competition, the visual reinforces why Brussels is tightening rules on platforms such as Shein, Temu, and AliExpress. At the same time, the inclusion of diplomatic imagery—handshakes and institutional symbols—reflects the dual-track nature of EU–China relations: cautious re-engagement alongside persistent structural disputes over market access, compliance, and economic reciprocity.

🇪🇺🇨🇳 EU Lawmakers Press China on Product Safety and Digital Trade

The European Parliament’s first visit to China in eight years has put a sharper spotlight on one of the most consequential issues in global trade today: how cross-border e-commerce is reshaping consumer safety,… pic.twitter.com/4z2Pc8TZdD

— European Hub for Contemporary China (@EuroHub4Sino) April 2, 2026

South Korea and France: A Strategic Partnership Shaped by Energy Shock and Security Convergence

Introduction

The decision by South Korea and France to elevate their relationship to a “global strategic partnership” is not just a ceremonial upgrade. It reflects a broader convergence driven by two pressures at once: the immediate disruption caused by the Iran war and the longer-term hardening of the international security environment. What gives the move significance is not simply that Seoul and Paris want closer ties, but that they are now linking defence, energy security, critical technologies, and maritime stability within one political framework. This is a more serious relationship than the label alone might suggest. The timing matters. The Iran war has exposed once again how vulnerable Asian and European economies remain to distant conflict, especially through energy chokepoints such as the Strait of Hormuz. At the same time, both South Korea and France face a wider strategic reality in which economic resilience and military capability can no longer be treated as separate domains. The partnership therefore reflects not diplomatic routine, but strategic adaptation.

Beyond Symbolism: Why the Upgrade Matters

There is always a risk of overstating these partnership declarations. This is not an alliance, and pretending otherwise would be sloppy. It creates no mutual defence commitment and does not fundamentally alter the military balance in Asia or Europe. But dismissing it as empty language would also be wrong. The substance lies in the sectors chosen for cooperation: defence, aerospace, semiconductors, critical minerals, quantum technology, nuclear energy, and offshore wind. That is a highly selective list, and it reveals what both governments think now matters most.

This is partnership-building around strategic capacity. In other words, South Korea and France are not merely expanding trade; they are trying to align in areas that affect national resilience, industrial competitiveness, and military relevance. The agreed ambition to increase bilateral trade is part of that story, but not the main point. The more important shift is the effort to build a denser relationship across industries that are increasingly tied to power politics.

Energy Security as Alliance Logic

One of the most important features of the upgrade is that it was explicitly linked to the disruption caused by the Iran war. That is significant because it shows how energy insecurity is now reshaping bilateral relationships that would once have been discussed primarily in commercial or diplomatic terms. Seoul and Paris agreed to cooperate on securing safe maritime transport through the Strait of Hormuz, which places energy transit and sea-lane security directly inside the logic of the partnership.

That makes sense. South Korea is acutely exposed to imported energy risk, while France has its own stake in protecting maritime order and preventing wider economic destabilisation. The partnership therefore reflects a shared recognition that energy shocks are not peripheral economic events. They are strategic tests. Once that is acknowledged, cooperation on maritime security, fuel supply, and industrial resilience becomes a natural extension of broader statecraft. The nuclear dimension reinforces this point. The memoranda involving Korea Hydro & Nuclear Power, Orano, and Framatome suggest that both sides want more than transactional cooperation. They are trying to strengthen nuclear fuel supply chains and potentially coordinate in overseas nuclear markets. That is not trivial. It means the partnership is beginning to connect energy security at home with industrial competition abroad.

Defence-Industrial Cooperation and Strategic Depth

The defence side of the partnership is equally important. Macron’s emphasis on joint exercises, production cooperation, and stronger “strategic depth” points to a relationship that is becoming more operational. Again, this should not be exaggerated. A handful of exercises or industrial projects does not produce a new strategic bloc. But it does matter that both countries are major arms producers and technologically capable military powers. Their cooperation is therefore not symbolic burden-sharing; it has the potential to generate real capability links.

This is especially relevant because both Europe and the Indo-Pacific are now being shaped by similar pressures: supply-chain insecurity, military modernisation, and the demand for more autonomous production capacity. South Korea brings advanced manufacturing, defence production, and technological scale. France brings military reach, nuclear expertise, and a more active Indo-Pacific role than many European states. The logic of deeper cooperation is obvious. What is emerging, then, is not a traditional alliance structure but a practical alignment between two states that see strategic value in reducing vulnerability while increasing industrial and military coordination. That is narrower than a formal alliance, but in current conditions it is also more realistic.

Conclusion

The South Korea–France partnership matters because it shows how regional alignments are changing. States are not only responding to threats through treaties or military postures; they are increasingly building security through technology, energy systems, industrial cooperation, and maritime coordination. That is what makes this upgrade more than diplomatic theatre.

Its significance should still be kept in proportion. It does not create a new axis, and it does not resolve the structural pressures either country faces. But it does show a clear trend: middle and major powers are drawing closer through selective partnerships designed to strengthen resilience in a more unstable world. South Korea and France are not forming an alliance in the classic sense. They are doing something more limited, but also more relevant to the present moment—building a strategic relationship around the intersection of energy shock, defence capability, and geopolitical uncertainty.

Japan’s Technology Strategy Is Becoming a Security Strategy

Introduction

The two latest investment moves in Japan—TSMC’s plan to produce 3-nanometre chips at its second Kumamoto plant and Microsoft’s $10 billion push into Japanese AI and cyber infrastructure—point to the same larger shift. Japan is no longer treating advanced technology primarily as an industrial policy issue. It is increasingly treating semiconductors, AI capacity, cloud infrastructure, and cyber resilience as part of national security. That is the real significance of these developments.

This matters because Japan has spent years trying to reduce strategic dependence without ever fully escaping it. It remains exposed to external supply shocks, to technological concentration in a handful of foreign firms, and to the geopolitical risks surrounding Taiwan and U.S.-China rivalry. The question now is not whether Japan can become technologically autonomous in any absolute sense—it cannot—but whether it can become less vulnerable in the sectors that matter most. These two developments suggest a more serious attempt to do exactly that.

Semiconductors: From Industrial Weakness to Strategic Reconstruction

TSMC’s decision to bring 3nm production to Japan is important because it moves the country beyond the lower-value role of hosting only mature-node manufacturing. That does not make Japan a peer of Taiwan in advanced chip production, and saying otherwise would be absurd. TSMC’s most advanced capabilities will still remain concentrated elsewhere. But the shift narrows the gap, and that alone is strategically meaningful.

Why? Because the semiconductor issue is not just about economic competitiveness. It is about concentration risk. Too much advanced chip capacity remains exposed to geopolitical pressure, above all around Taiwan. For Japan, attracting higher-end production is therefore a hedge against disruption and a way to regain relevance in a sector it once dominated but later allowed to erode. Kumamoto is not simply a factory story. It is part of a wider redistribution of strategically important production across the Indo-Pacific.

The U.S. angle also matters. Japan’s semiconductor recovery is not unfolding in isolation, but within a broader alignment among Washington and its partners to diversify high-end production and reduce dependence on insecure concentrations. That does not amount to full “de-risking” in any clean sense, because supply chains remain global and deeply entangled. But it does show a clear effort to make the geography of chip production less brittle.

AI Infrastructure: Commercial Expansion with Security Logic

Microsoft’s Japan investment reflects a similar pattern in a different sector. On the surface, this is a corporate growth story: more cloud capacity, more AI adoption, more training, more computing infrastructure. But that reading is too narrow. The more important point is that AI infrastructure is being anchored physically and institutionally inside Japan, with explicit links to cybersecurity cooperation and public-sector resilience.

That is a security development, not merely a business one. The emphasis on keeping sensitive government and corporate data in Japan while still using Microsoft’s systems speaks directly to concerns about jurisdiction, exposure, and control. In other words, Japan is trying to capture the benefits of foreign technological scale without surrendering too much operational sovereignty. That is a rational approach, even if it remains incomplete.

The labour component is also more significant than it first appears. Training one million engineers and developers is not just about filling jobs. It is about expanding the domestic human base needed to operate and secure advanced digital systems. A country facing a major projected shortfall in AI and robotics talent cannot seriously talk about technological resilience if it lacks the people to sustain it.

The Limits of Japan’s Strategy

Still, this emerging model has obvious limits. Japan is strengthening its technological position, but largely through dependence on foreign firms—TSMC in semiconductors, Microsoft in AI and cloud infrastructure. That is not sovereignty in any pure sense. It is managed dependence. The Japanese state appears to have accepted that complete self-sufficiency is unrealistic and is instead trying to secure preferential embedding within allied or trusted technology networks.

That may be the only realistic option, but it carries risks. Foreign investment can deepen local capacity, yet it also leaves core infrastructure tied to external corporate decisions and broader geopolitical shifts. Japan is becoming more resilient, but not independent. That distinction matters, and anyone blurring it is not thinking clearly.

Conclusion

Taken together, these developments show that Japan’s technology policy is hardening into strategic policy. Advanced chipmaking, AI infrastructure, domestic data capacity, cyber cooperation, and workforce development are increasingly being treated as components of national resilience rather than separate economic goals. This is not a dramatic break, but a cumulative reorientation.

The broader lesson is straightforward. In today’s environment, states do not secure themselves only through ships, missiles, and alliances. They also do so through fabs, cloud architecture, talent pipelines, and control over sensitive digital systems. Japan appears to understand that more clearly than before. The question is whether managed dependence on trusted foreign firms will prove durable enough in a world where technology is no longer just a source of growth, but a terrain of strategic competition.