INTRODUCTION

In March 2023, China brokered a historic rapprochement between Saudi Arabia and Iran —two regional rivals whose antagonism had long shaped Middle Eastern geopolitics (Fulton, 2021). This Beijing-mediated agreement, which restored diplomatic relations severed in 2016, raised fundamental questions about the evolving architecture of global power and China’s growing influence in the Gulf.

To explore these dynamics, this study focuses on three Gulf countries—Saudi Arabia, the United Arab Emirates, and Iran—that represent contrasting types of Chinese economic engagement and political alignment. Saudi Arabia and the UAE are key economic partners of both China and the West, reflecting different degrees of economic dependence and strategic flexibility. Iran, by contrast, is subject to extensive international sanctions and relies heavily on China as an economic and political partner out of necessity. This comparative design enables a nuanced analysis of how economic statecraft operates across diverse regional contexts.

Unlike traditional Western powers, China has no military presence in the region but has systematically expanded its economic footprint. Over the past decade, China has become Saudi Arabia’s largest trading partner (Fulton, 2019), the UAE’s main source of non-oil trade growth, and Iran’s economic lifeline despite sanctions (Fulton, 2020). Chinese foreign direct investment and bilateral trade volumes have increased exponentially, reshaping infrastructure and economic interdependence.

Yet, the link between this economic engagement and political alignment remains complex. The Gulf states, while maintaining deep security partnerships with the United States, increasingly align politically with China in selective and strategic ways.

This article investigates how China’s economic instruments translate into political influence in the Gulf and why the conventional assumption, that economic dependence directly predicts political alignment, does not fully explain the observed patterns. Emphasis is placed on the interplay between economic incentives and strategic, institutional, and geopolitical mediators shaping the outcomes.

China’s Economic Statecraft in the Gulf: Tools and Initiatives

China’s expanding presence in the Gulf builds on a deep historical relationship and strategic imperatives related to energy security and multilateral diplomacy (Leung, 2011). Unlike traditional powers, China relies on a complex portfolio of economic instruments rather than military means to exert influence.

Historical and Strategic Context

China’s relations with the Middle East trace back to ancient Silk Road interactions, but have intensified recently due to China’s rising global economic power and its urgent energy needs (Shichor, 2018). The Gulf region’s strategic location—at the crossroads of Asia, Africa, and Europe—and its vast hydrocarbon resources make it central to China’s global strategy. China also pursues a “periphery diplomacy” (周边外交 - zhōubiān wàijiāo) aimed at regional stabilization through infrastructure development and hedging against geopolitical risks via multilateral institutions (Swaine, 2014).

Economic Instruments Deployed

China’s economic statecraft in the Gulf involves multiple complementary tools:

- Foreign Direct Investment (FDI): China channels investments into key sectors including energy, petrochemicals, transportation, and technology. This creates long-term entanglements and economic dependencies.

- Loans and Infrastructure Financing: state-owned banks like China Development Bank and Eximbank extend credit for large infrastructure projects, supporting energy terminals, ports, industrial zones, and transportation corridors under Belt and Road Initiative (BRI) frameworks (Gelpern et al., 2021; Horn et al., 2021).

- Currency Swaps and Bilateral Financial Agreements: RMB currency swap agreements with Gulf countries, including Saudi Arabia and the UAE, facilitate trade settlement in Chinese currency and support RMB internationalization, a strategic objective linked to reducing reliance on the US dollar.

- Multilateral Financial Institutions: the Asian Infrastructure Investment Bank (AIIB) provides a platform for financing projects aligned with China’s geopolitical objectives, emphasizing connectivity, infrastructure, and energy development in the Gulf.

- Trade Agreements and Tariff Policies: China pursues preferential trade agreements with Gulf Cooperation Council (GCC) countries, institutionalizing economic relations and promoting a political narrative of mutual benefit and sovereignty.

Gulf States’ Participation in Chinese-Led Initiatives

Gulf countries actively engage in China-led economic initiatives, signaling institutional alignment beyond bilateral relations:

- Participation in the AIIB reflects strategic openness to China’s multilateral financial apparatus.

- OPEC+ coordination with China influences global energy governance despite China’s non-membership.

- The Belt and Road Initiative serves as an extensive platform for infrastructure diplomacy, embedding Gulf states in China’s global economic network.

Asymmetrical Interdependence

While cooperation appears mutually beneficial, inherent asymmetries favor China strategically. These asymmetries create structural economic dependencies that condition political behavior over time without explicit coercion, a dynamic known as “vulnerability interdependence.” Gulf states, while maintaining agency, face increasing opportunity costs associated with misalignment.

Case Studies: Saudi Arabia, UAE, and Iran

This chapter examines how China’s economic statecraft operates across three Gulf countries with distinct strategic positions, economic structures, and geopolitical constraints. The analysis reveals that economic engagement creates conditions for political alignment, but the depth and nature of that alignment vary significantly based on state capacity, strategic vision, and security environments.

Saudi Arabia

Saudi Arabia exemplifies what can be termed “calibrated engagement”—a deliberate strategy of deepening institutional and economic ties with China while maintaining traditional security partnerships with the United States.

Chinese FDI in Saudi Arabia increased from $1.99 billion in 2014 to $3.52 billion in 2021, before settling down to $3.19 billion in 2023 (ChinaMed, n.d.). This volatility reflects the Kingdom’s strategic calculations amid intensifying US-China competition rather than purely commercial dynamics. Most of the Chinese FDI has been concentrated in the energy sector (China Customs Statistics, 2014), underscoring China’s strategic focus on resources critical to its economic security.

Table 1. Chinese FDI Stock in Saudi Arabia (2014–2023, USD billions) – Source: World Bank

Bilateral trade has grown steadily, with China consistently absorbing over 76% of Saudi oil exports during the analyzed period. Saudi Arabia’s trade dependency on China averages 8.35% of GDP over the decade (OEC, n.d.), reflecting substantial but not overwhelming economic integration.

Saudi Arabia’s political convergence with China accelerated markedly following Vision 2030’s launch. The Kingdom introduced Mandarin into national school curricula (Alshammari, 2024)—a symbolic signal of long-term strategic reorientation; in 2019, Riyadh co-signed UN letters defending Chinese policies in Xinjiang and in August 2023 it was accepted into BRICS expansion and approved Shanghai Cooperation Organization membership (Nebehay, 2019). This alignment reflects deliberate strategic choices linked to domestic transformation objectives rather than economic coercion.

United Arab Emirates

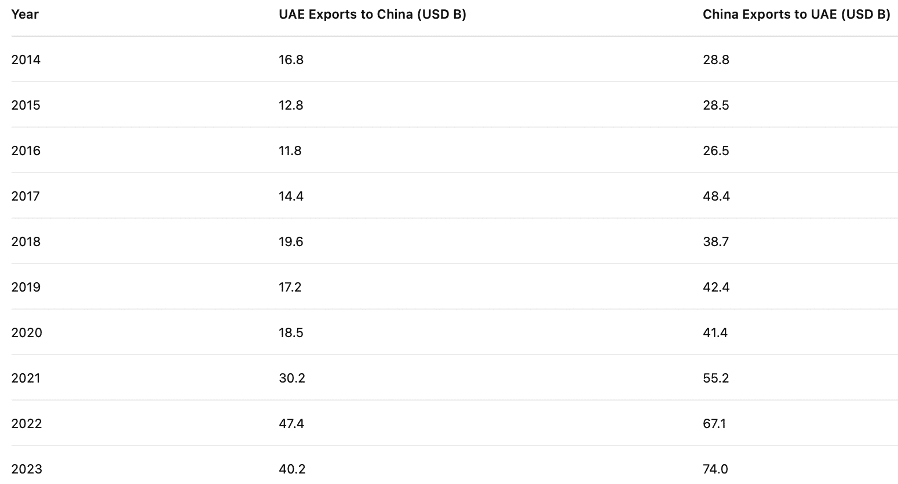

The UAE demonstrates the highest economic dependence on China among the three cases, yet paradoxically maintains the greatest strategic autonomy—exemplifying sophisticated compartmentalization of economic and security relationships.

Chinese FDI stock in the UAE grew from $1.36 billion in 2014 to $9.56 billion in 2023 (ChinaMed, n.d.)—a nearly sevenfold increase. Bilateral trade represents on average 15.92% of Emirati GDP (OEC, n.d.), the highest level among the three countries. This elevated trade exposure reflects the UAE’s role as a regional commercial hub and re-export center embedded in China’s Belt and Road logistics networks.

Table 2. Chinese FDI Stock in UAE (2014–2023, USD billions) – Source: World Bank

Table 3. Total Bilateral Trade between China and the UAE (2014–2023) – Source: OEC

Despite high economic integration, the UAE maintains sophisticated strategic hedging. Abu Dhabi supports China on selective issues like Hong Kong and Xinjiang but preserves robust Western security partnerships and demonstrates flexibility in UN forums. The UAE’s 2023 BRICS+ invitation signals confidence in managing multiple institutional commitments without compromising core relationships (Asia Dialogue, 2020). This reflects superior institutional capacity to manage complex interdependence through economic diversification and strategic portfolio balancing.

Iran

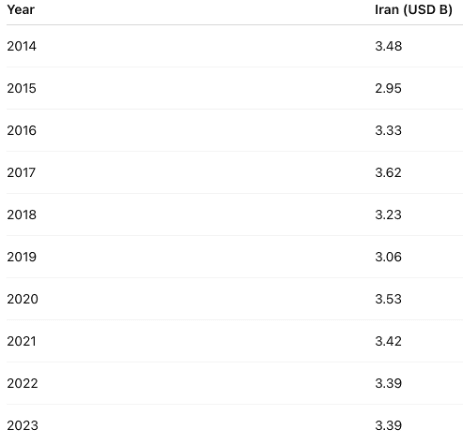

Iran presents a fundamentally different profile: the lowest measured economic dependence yet the most comprehensive political alignment with China. This pattern reflects strategic necessity driven by Western sanctions rather than economic vulnerability per se.

Economic Integration: Iran’s Chinese FDI stock remained relatively stagnant between $3-4 billion throughout 2014-2023 (U.S. EIA, 2014), despite the $400 billion strategic cooperation agreement signed in 2021. Western sanctions have structurally limited formal economic integration.

Table 4. Chinese FDI Stock in Iran (2014–2023, USD billions) – Source: World Bank

Despite modest economic integration, Iran demonstrates the most extensive political alignment. Tehran has embraced Chinese institutional frameworks, adopted Beijing’s diplomatic rhetoric, and systematically aligned with Chinese positions in international forums. In July 2019, Iran publicly defended Chinese policies in Xinjiang at the UN Human Rights Council. This comprehensive alignment emerges not from economic dependence but from sanctions-induced isolation that eliminates alternative partnerships, making China Iran’s only viable strategic partner.

Comparative Analysis: Explaining Variation

The three cases reveal that economic engagement establishes foundations for political alignment, but the relationship is mediated by four key factors:

- State Capacity: the UAE’s superior institutional sophistication allows management of complex interdependence while maintaining strategic flexibility despite high economic dependence.

- Strategic Vision: Saudi Arabia has integrated Chinese cooperation into Vision 2030, creating domestic momentum and constituencies that reinforce alignment beyond immediate economic incentives.

- Security Constraints: Iran’s comprehensive alignment reflects strategic necessity under sanctions rather than economic vulnerability, demonstrating that political alignment can emerge from geopolitical isolation.

- Geopolitical Opportunities: great power competition offers Gulf states leverage to balance economic benefits with political flexibility—those with greater capacity exploit this more effectively.

Economic Dependency Index (EDEP)

The Economic Dependency Index (EDEP) was developed to capture and compare the degree of economic reliance on China among Saudi Arabia, the United Arab Emirates, and Iran during 2014–2023. It serves as a systematic, quantitative tool to highlight structural economic dependencies that may shape political alignment.

Index Components:

The EDEP combines two key indicators:

- Chinese Foreign Direct Investment (FDI) stock: capturing long-term economic entanglement and strategic positioning.

- Bilateral trade volume: measured as the sum of imports and exports with China, reflecting economic integration and exposure.

Both variables are used as a share of each country’s GDP for comparability across time and countries.

Table 5. Economic Dependency Index: aggregated results – Author’s elaboration based on FDI stock and trade as % of GDP

Excluded Variables and Limitations:

Attempts to include Chinese loans and debt shares as a percentage of GDP were abandoned due to the lack of consistent, granular, and transparent longitudinal data—especially for Iran, but also for Gulf monarchies where financing often takes the form of joint ventures or non-public agreements. This exclusion is crucial: while loans and debt would portray an even greater degree of dependency for some states, omitting them ensures the robustness of the index given available data.

Method of Construction:

Raw annual values of Chinese FDI stock and bilateral trade with China were first collected for each country and year in the 2014–2023 period. These series were then rescaled to a common 0–1 range through min–max normalization, ensuring comparability across countries and over time. The EDEP for each country‑year is calculated as the simple arithmetic mean of the normalized FDI and trade indicators, assigning equal weight to both components.

Benchmarking Economic Dependency: the Case of Cambodia

In order to better contextualize the values of economic dependency calculated for the Gulf countries, this study adopts Cambodia as a benchmark country. Cambodia is widely recognized as one of the states most economically reliant on China—both in terms of trade and foreign direct investment. Several sources, including the Lowy Institute Asia Power Index, academic studies on Sino-Cambodian relations, and reports from CSIS and Brookings Institution, consistently highlight Cambodia’s deep integration into China’s economic sphere, often citing it as an archetype of Chinese economic statecraft in Southeast Asia.

Using Cambodia’s ten-year average ratios of Chinese FDI stock and bilateral trade as a percentage of GDP (2.18% and 26.57%, respectively) as reference (100%), the scores previously calculated for Saudi Arabia, the UAE, and Iran were normalized on a scale from 0 to 1. This allows for an intuitive comparative interpretation: a normalized score of 1 would indicate a level of economic dependency comparable to that of Cambodia—arguably the upper bound of contemporary economic entanglement with China.

Table 13. Economic Dependency Index: normalized results – Author’s elaboration based on Cambodia’s reference ratios (FDI stock 2.18% of GDP; Trade 26.57% of GDP)

Correlation Between Chinese Economic Instruments and Political Alignment

This section moves beyond descriptive metrics and investigates whether—and how—economic dependence on China translates into observable political alignment among Saudi Arabia, the United Arab Emirates, and Iran across four key dimensions:

- Voting behavior at the United Nations

- Participation in China-led institutions

- Official rhetoric and diplomatic discourse

- Strategic positioning vis-à-vis the United States

Empirical analysis reveals that economic engagement consistently establishes a permissive foundation for political alignment, but the depth and character of alignment are shaped by mediating factors that quantitative measures alone do not capture (Zhao, 2022).

Iran exhibits the highest degree of political alignment with China across every dimension—consistent UN voting, rhetorical convergence, and institutional participation—despite having the lowest formal EDEP score. Here, alignment is primarily explained by strategic necessity and the absence of Western alternatives due to sanctions.

Saudi Arabia sits at an intermediate EDEP level, but demonstrates a clear trend toward deeper political alignment, as evidenced by joining BRICS+, opening to educational cooperation, and accelerating institutional agreements. Political alignment is driven by deliberate national transformation objectives, especially Vision 2030, and reflects both material incentives and long-term strategic vision.

UAE holds the highest EDEP, embodying maximum economic integration but maintains significant strategic autonomy. The UAE compartmentalizes support for China on selective issues, preserves Western security ties, and exhibits flexibility in international forums—a result of state capacity, diversification, and hedging strategies.

This nuanced pattern implies that while Chinese economic instruments create room for alignment, actual political behavior is mediated by factors such as institutional capacity, domestic transformation projects, security context, and geopolitical opportunity structures.

The findings challenge the linear and deterministic assumption often found in international political economy literature: higher economic dependence does not directly or proportionally generate higher political alignment.

Political alignment can emerge from strategic constraints (sanctions, isolation), not only from economic vulnerability. Conversely, high economic dependence, when paired with robust institutional capacity, can be leveraged for autonomy and hedging rather than subservience.

Conclusion

This article advances a nuanced understanding of how China’s economic engagement translates into political influence in the Gulf. China’s presence is now a structural reality, making it a key actor in the region’s economic growth and strategic diversification. Yet, the link between economic dependence and political alignment is mediated by state capacity, strategic vision, security environment, and regional competition.

The Gulf cases demonstrate that economic engagement by a great power creates permissive conditions for alignment, but material advantage alone is insufficient for sustained influence. China’s most effective statecraft leverages the unique context of each partner, creating stakeholder constituencies, institutional dependencies, and policy path dependencies that interact with domestic reform agendas and shifting geopolitical realities.

In other words, Chinese economic statecraft does not guarantee political obedience; instead, it expands the range of options for Gulf states to reposition themselves in a rapidly changing world, supporting hedging, diversification, and, in some cases, convergence.

The complexity, non‑linearity, and context‑dependence of this relationship have critical implications for both theory and practice, suggesting that influence in the 21st‑century Gulf will depend more on sophisticated economic diplomacy than on military presence or simple trade volume (Baldwin, 2016). In this sense, the Gulf is not just a recipient of Chinese economic statecraft but a laboratory where new rules of great‑power competition are being tested, negotiated, and resisted, offering a preview of how “geoeconomics” is shaping the international order.

REFERENCES

Alshammari, H. (2024) ‘Saudi Arabia begins Chinese-language classes at schools’, Arab News, 10 September. Available at: https://www.arabnews.com/node/2570858/amp (Accessed: July 2025).

Asia Dialogue (2020) ‘China’s partnership diplomacy in the Middle East’. [Online]. (Accessed: July 2025).

Asian Infrastructure Investment Bank (AIIB) (2025) ‘AIIB official data on country shares and voting rights’. Available at: https://www.aiib.org/en/about-aiib/governance/members-of-bank/index.html (Accessed: July 2025).

Baldwin, D.A. (1985) Economic Statecraft. Princeton, NJ: Princeton University Press.

Baldwin, D.A. (2016) Power and International Relations: A Conceptual Approach. Princeton, NJ: Princeton University Press.

Bayne, N. and Woolcock, S. (2017) The New Economic Diplomacy: Decision-Making and Negotiation in International Economic Relations (4th ed.). London: Routledge.

Blanchard, J-M.F. (2009) ‘A Political Theory of Economic Statecraft’, in Blanchard, J-M.F., Dombrowski, E.D. and Kirshner, D.A. (eds) Power and the Purse: Economic Statecraft, Interdependence, and National Security. London: Routledge, pp. 371–393.

Blanchard, J-M.F. and Murshed, S.M. (2016) ‘The Political Economy of China’s Infrastructure Diplomacy’, The China Review, 16(1), pp. 1–26.

Calabrese, J. (2018) ‘China’s “One Belt, One Road” (OBOR) Initiative: Envisioning Iran’s Role’, in Ehteshami, A. and Horesh, N. (eds) China’s Presence in the Middle East: The Implications of the One Belt, One Road Initiative. London: Routledge, pp. 173–184.

CEIC Data (n.d.) ‘China: ODI: Asia: Cambodia’. Available at: https://www.ceicdata.com/en/china/outward-direct-investment-by-country/outward-investment-asia-cambodia (Accessed: July 2025).

China Customs Statistics (2014) ‘China’s Top Sources of Crude Oil’. Available at: https://www.customs.gov.cn (Accessed: July 2025).

ChinaMed (n.d.) ‘ChinaMed Data – Middle East’. Available at: https://www.chinamed.it/chinamed-data/middle-east (Accessed: July 2025).

Fulton, J. (2019) ‘China’s Changing Role in the Middle East’, Atlantic Council. Available at: https://www.atlanticcouncil.org (Accessed: July 2025).

Fulton, J. (2020) ‘China’s changing role in the Middle East’, Atlantic Council Issue Brief, October. Available at: https://www.atlanticcouncil.org/in-depth-research-reports/issue-brief/chinas-changing-role-in-the-middle-east/ (Accessed: 10 July 2025).

Fulton, J. (2021) ‘China and the Persian Gulf in the Age of the BRI: The View from the Gulf’, in Zoubir, Y.H. (ed.) The Politics of China’s Belt and Road Initiative. Cham: Palgrave Macmillan, pp. 207–228.

Gelpern, A., Horn, S., Morris, S., Parks, B. and Trebesch, C. (2021) How China Lends: A Rare Look into 100 Debt Contracts with Foreign Governments. Williamsburg, VA: AidData at William & Mary.

Horn, S., Reinhart, C.M. and Trebesch, C. (2021) ‘China’s Overseas Lending’, Journal of International Economics, 133, 103539.

Huang, J. (2025) ‘A Comparative Analysis of China’s New Era Economic Diplomacy and the Economic Diplomacy Strategy of the Biden Administration’, Journal of Modern Social Sciences, 2(2), pp. 126–131. https://doi.org/10.71113/JMSS.v2i2.257

Keohane, R.O. and Nye, J.S. (1977) Power and Interdependence: World Politics in Transition. Boston, MA: Little, Brown.

Keohane, R.O. and Nye, J.S. (2012) Power and Interdependence (4th ed.). Boston, MA: Pearson.

Leung, G.C.K. (2011) ‘China’s energy security, the Malacca dilemma and responses’, Energy Policy, 39(12), pp. 7612–7615.

Mearsheimer, J.J. (2001) The Tragedy of Great Power Politics. New York: W.W. Norton.

Nebehay, S. (2019) ‘Saudi Arabia and Russia among 37 states backing China’s Xinjiang policy’, Reuters, 12 July. Available at: https://www.reuters.com/world/saudi-arabia-and-russia-among-37-states-backing-chinas-xinjiang-policy-idUSKCN1UA1FD/ (Accessed: July 2025).

Nye, J.S. (2004) Soft Power: The Means to Success in World Politics. New York: PublicAffairs.

Nye, J.S. (2011) The Future of Power. New York: PublicAffairs.

Observatory of Economic Complexity (OEC) (n.d.) ‘OEC Data Portal’. Available at: https://oec.world/ (Accessed: July 2025).

Shichor, Y. (2018) ‘China’s Presence in the Middle East: Vision, Revision and Supervision’, in Ehteshami, A. and Horesh, N. (eds) China’s Presence in the Middle East. London: Routledge.

Swaine, M.D. (2014). Chinese Views and Commentary on Periphery Diplomacy. Carnegie Endowment.

Strange, S. (1988) States and Markets: An Introduction to International Political Economy (2nd ed.). London: Continuum.

Strange, S. (1994) ‘Wake Up, Krasner! The World Has Changed’, Review of International Political Economy, 1(2), pp. 209–219.

U.S. Energy Information Administration (EIA) (2014) ‘Iran’s Oil Exports by Destination’. Available at: https://www.eia.gov (Accessed: July 2025).

Woolcock, S. (2017) ‘Factors Shaping Economic Diplomacy: An Analytical Toolkit’, in Bayne, N. and Woolcock, S. (eds) The New Economic Diplomacy (4th ed.). London: Routledge.

Zhao, S. (2022) ‘China’s Hedging Strategy in the Middle East: Balancing Relations with Competing Regional Powers’, Journal of Contemporary China, 31(137), pp. 251–268.